Draft Summary of Discussion

For Borrowers in Trouble: Partial Payments

Skip to issuePlease take a few minutes to fill out this SHORT survey about your Regulation Room experience, it should take less than 10 minutes. Your feedback is important to our work in expanding public understanding and meaningful participation in government policymaking. To show our appreciation for your help, two people who respond by November 1 will receive $50 gift certificates to Amazon.com.

§1. What’s going on here?

This is a summary of discussion on the “For Borrowers in Trouble: Partial Payments” post from August 10 to October 3, 2012. (On that date, the post was closed to further discussion.) It was written by the Regulation Room team. This version is a DRAFT. Please help make sure that nothing is missing, wrong, or unclear. You can propose changes to this version until October 8.

The goal is to give CFPB the best possible picture of the different views, concerns, and ideas that came out during the discussion. This is NOT the place to reargue your position or criticize a different one. Focus on whether anything is missing or unclear, not whether you agree or disagree.

On October 9, the Final Summary will be posted on Regulation Room and submitted to CFPB as a formal comment in the official rulemaking record. (October 9 is the last day of the official commenting period.)

Please take a few minutes to fill out this SHORT survey about your Regulation Room experience, it should take less than 10 minutes. Your feedback is important to our work in expanding public understanding and meaningful participation in government policymaking. To show our appreciation for your help, two people who respond by November 1 will receive $50 gift certificates to Amazon.com.

§2. What should happen with partial payments

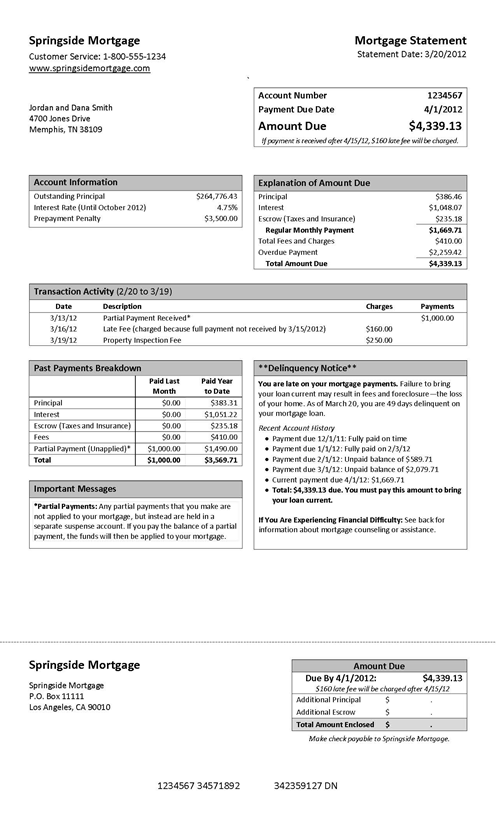

Four commenters urged CFPB to require that servicers accept partial payments and apply them to the loan balance even before they add up to a full payment.

One, a consumer who also worked for a servicer, recounted her own experience:

“I had an instance where we had some medical things happen and I knew I was going to be late on a payment and called the servicer prior to the payment being due and was told there was nothing they could talk to me about and recommended I let the loan go past due! I had the funds to make 2/3′s of the payment but unless it was a full payment they wouldn’t accept it. I was horrified by this and the service I received.”

The commenter contrasted this with the practice of his/her previous employer who serviced loans and accepted late payments. This employer’s goal was to get the loan current and avoid foreclosure. The late fee ($25 if the loan was 10 days past due) was the last thing collected and could be waived if a plan to get the loan current was made with the client. Their practice was to make a payment reminder and call to the client after the account became 10 days past due. The servicer’s representative would discuss the situation with the client and propose options to get the account back on track (the commenter noted in his/her experience that a majority of consumers want to find a solution and just need help). If a plan was agreed upon, the servicer followed up with a letter to the client and necessary documents were signed, even if the loan was 30 days past due. Based on this experience, the commenter wrote: “I understand that at a certain point when a loan is past due if the lender is continuing the foreclosure process … they cannot accept payments; however I do not understand why they can’t accept partial payments and apply them to the loan. By not accepting the payment unfortunately what happens is people pay something else that has to be paid.” S/he argued that it is wrong for servicers to refuse to accept partial payments and advise borrowers not to make them; moreover, since foreclosure is expensive for the lender, it would often be less expensive for the servicer to take the payment and work with the borrower.

Another commenter (a consumer with personal or family experience with foreclosure, in a household making less than $100,000/year) recounted the experience of being “told I hadn’t made a payment even when I had, and that it ‘didn’t count’ even [though] there were 2 months of suspense fund payments present.” This commenter argues that servicers don’t accept partial payments on government backed loans (like FHA) because it maximizes mortgage-insurance claims: they are more interested in getting an insurance claim for a mortgage than avoiding default, because the claim is worth more than the foreclosed property due to market value changes. S/he urges that lenders who do not accept and immediately credit partial payments “should forfeit their right to make a claim on a [government] backed mortgage.”

The third commenter (a consumer who expects to be a first-time home buyer in the next few years and whose household makes less than $100,000 per year) wondered, after studying the sample periodic statement, why the lender can’t apply as much of the partial payment as is needed to bring a late payment up-to-date. S/he suggested that, when a borrower makes a partial payment that is less than one full installment, lenders should be required to credit the payment to the amount the borrower owes. At the least, the partial payment should be held in a suspense account that “pays interest on the funds equal to the interest on the loan.” Otherwise consumers have no incentive to make a partial payment. Also, returning a partial payment encourages the borrower to use the money for something else (especially if the borrower is “in a financial bind.”) “To hold funds in the suspense account until the full amount is collected and fees are paid still hurts the borrower who is at least trying to catch up. Even paying interest and then the remainder to principal on a partial payment helps the borrower catch up.” If partial payments are accepted, the borrower at least gets some credit for attempting to fulfill his or her obligation. The commenter believed the increased recordkeeping created by this change for servicers would be minimal, certainly not any more difficult than keeping track of the partial payments in a suspense account. Hitting a theme that ran through the discussion as a whole, s/he suggested that software technology could make the allocations “automatically or nearly so.”

A fourth commenter (consumer with personal or family experience with foreclosure) agreed that “partial payments can be part of the solution and maybe even the determining factor in bringing the borrowers loan current by allowing additional time. ”

§3. Disclosure to borrowers

Commenters agreed that the policy on and impact of partial payments should be disclosed. One commenter, who had worked for an insurance company whose clients came from all over the country and/or other countries, approved of the way the sample periodic statement treated special disclosures about suspense accounts, but emphasized that the rule should require that the same information be provided to borrowers whenever and however they contact their servicer – whether online, over the phone, or in person.

{kind=link}

§4. Treatment of late fees

A small lender commenter (self-identified as mortgage servicer/originator/owner whose company’s customers are mostly from the local community) provided a sharply contrasting view. Specifically addressing late fees, this commenter more generally urged CFPB to take a principled approach that respects the contractual nature of mortgages:

“Should the late charge be included as part of what is considered a full monthly payment? The answer to this question needs to be guided by the long history of contract law in America. If the customer makes his payment after the grace period has expired, then the customer is contractually obligated to pay the late charge. So the answer is yes, the customer must pay the late charge before the monthly payment is to be considered fully paid. The CFPB should not be issuing a rule which over-rides a legal contractual obligation of the borrower to the lender. Excluding the late charge is arbitrary and not based on any solid legal foundation. It just feels good. The rule could just as well exclude the principal portion of the payment and include only the past due interest. Why not? Excluding the principal portion is no more arbitrary than excluding the late charge.

“Please make rules which are based on the legal contractual obligation between the borrower and the lender, not based upon a feel good approach that views lenders and loan servicers as evil and borrowers as angels that are never in the wrong and have no responsibilities to live up to.”